If you have an apartment in Japan, your “fire disaster insurance” may also be toilet insurance

Got a busted toilet in your place in Japan? Check for this before you pay the whole repair bill.

When moving into a new apartment in Japan, there are a lot of different payments you have to make. There’s the first and last month’s rent, security deposit, real estate agency fee, the one-time move-in fee paid to the landlord called “key money,” and the fee for actually changing the locks and making new keys. So by the time you get to the part of the process where you’re required to pay for “fire disaster insurance,” you’ll probably just shrug your shoulders and say “Yeah, that makes sense” without reading all of the fine print.

But here’s the thing about “fire disaster insurance”: it doesn’t just cover you against fire damage, and sometimes it also works as toilet insurance.

First, let’s take a quick look at the linguistics for this required insurance for renters. In Japanese it’s called kasai hoken, which is written in kanji like this.

This does literally translate as “fire disaster insurance.” The first kanji, 火, means “fire,” and the second 災, is “disaster.” Together they become 火災, kasai, meaning a destructive fire (as opposed to, say, a cooking fire or campfire). And 保険/hoken is the Japanese word for “insurance.”

But even though the name only mentions fire, kasai hoken is really an umbrella policy that covers all sorts of unpleasant situations. In addition to fire, it also usually functions as insurance against flood, wind, snow, hail, and water damage, and sometimes even certain instances of damage as a result of flying object impact and theft. And as we mentioned above, your “fire disaster insurance” may also cover damage to bathroom fixtures like your bathtub, washbasin, and toilet.

We found this out recently when one of our Japanese-language reporters, Ahiruneko, was moving out of his old apartment, which got him thinking about his recently broken toilet seat.

Since the bowl itself is OK, Ahiruneko had just kept on using the toilet without getting the seat fixed. As part of the process of moving out, though, the landlord would be doing a final check of the apartment, and Ahiruneko figured the cost of the toilet repairs was going to come out of his deposit. What’s worse, since it’s a fancy washlet-style toilet, he figured it wasn’t going to be cheap to fix.

So he asked his landlord whether repair costs for the toilet might be covered under his kasai hoken policy. The landlord told him he’d have to check with the insurance provider, so that was the next call Ahiruneko made, and to his happy surprise, they told him that yep, his “fire disaster insurance” also works as toilet insurance.

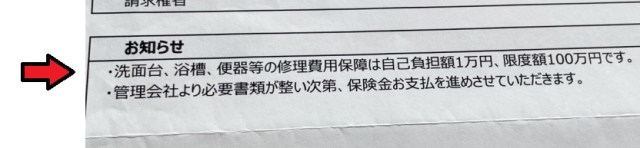

The section of Ahiruneko’s insurance contract that the arrow is pointing to in the above photo indicates that repair costs of up to one million yen (US$6,850) for his apartment’s toilet, washbasin, or bathtub are covered, with Ahiruneko having to pay just 10,000 yen out of his own pocket. This turned out to be great news, because when the landlord came by for his pre-move-out inspection, they assessed that it was going to cost 28,000 yen to repair the toilet.

So in the end, Ahiruneko’s “fire disaster insurance” ended up saving him 18,000 yen in toilet repairs, more than half the total bill.

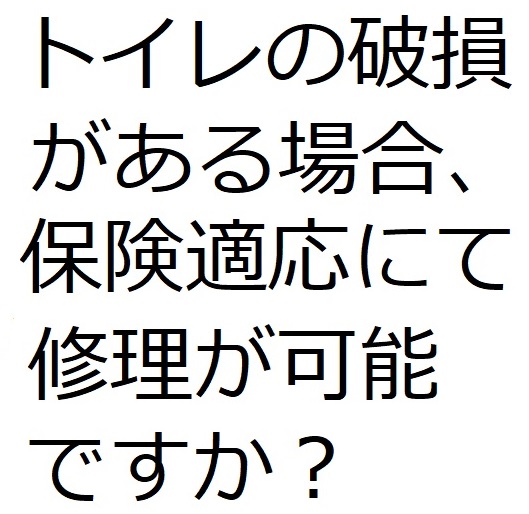

We should note that the exact details of kasai hoken coverage may vary by insurance provider. If you want to check if yours will cover toilet repairs, you can ask the customer service rep “Toire no hason ga aru baai, hoken tekiou nite shuuri ga kanou desu ka?”, which means “In the case of damage to the toilet, can my insurance be applied to the repairs?”

▼ That same phrase, written in Japanese

If you want to change that to asking about the bathtub, all you have to do is swap out toire (トイレ) and put in yokusou (浴槽), and if you’re asking about the washbasin, the word to use is senmendai (洗面台).

If the fixture that needs fixing is covered by your insurance, the exact process for filing the claim also may vary by provider, but in general you’ll need a document confirming the repair cost from your landlord, which will then need to be supplied to your insurance provider. In Ahiruneko’s case, he ended up having the full repair cost of 28,000 yen deducted from his security deposit, and after that he received a notice from his insurance provider saying that they had approved his claim and sent the money to his landlord, who then transferred the money into his bank account. With all that sorted out, though, he’s got 18,000 extra yen in his pocket, and he’s thankful that his “fire disaster insurance” kept him from getting burned for the full repair bill.

Reference: General Insurance Association of Japan

Images ©SoraNews24

● Want to hear about SoraNews24’s latest articles as soon as they’re published? Follow us on Facebook and Twitter!

Credit:

0 comments:

Post a Comment